API Overview

The sscmfiAPI suite consists of ten high-performance endpoints designed to handle complex fixed income calculations with precision.

API Integration Workflow

/api/sscmfiPublicAPI

Available for public use, this endpoint offers the same powerful functionality as our calculation suite. It is rate-limited and governed by our Terms of Service. Perfect for testing and small-scale integrations.

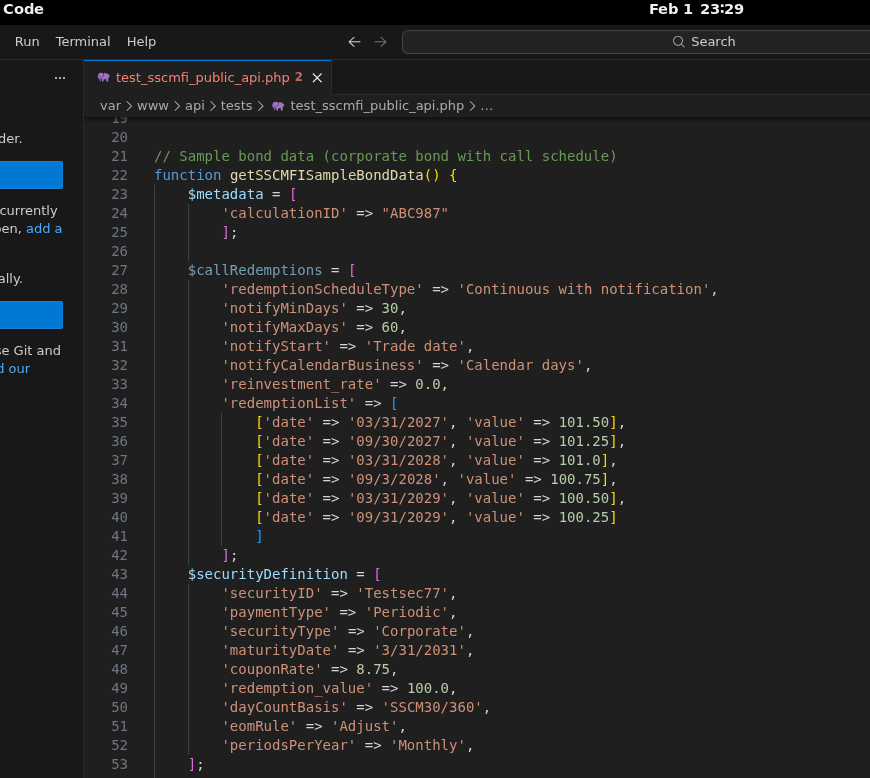

The sscmfiAPI documentation workflow provides a structured approach to integrating bond math into your stack. From exploring schemas in Swagger UI to benchmarking results with our live calculator, we provide the tools you need for a seamless implementation.

Subscription API Suite

/api/sscmfiAPICalculateCan perform any of the supported calculations for any of the supported payment types.

/api/sscmfiAPIBatchCalculatePerforms the same calculations as sscmfiAPICalculate with the performance boost of batching together up to 1000 requests.

/api/sscmfiAPICalculatePeriodicPerforms calculations for fixed coupon rate securities paying periodically.

/api/sscmfiAPICalculateDiscountPerforms calculations for discount securities paying at maturity.

/api/sscmfiAPICalculateIAMPerforms calculations for fixed coupon rate securities with a single payment at maturity.

/api/sscmfiAPICalculateSteppedPerforms calculations for securities with stepped coupon rates.

/api/sscmfiAPICalculateMultistepPerforms calculations for securities with multiple fixed coupon rate changes.

/api/sscmfiAPICalculatePIKPerforms calculations for Payment-In-Kind (PIK) securities.

/api/sscmfiAPICalculatePartPIKPerforms calculations for part cash, part PIK coupon securities.

Calculation Results Control

Customize your response by setting the following boolean flags to "Yes":

Price & Yield

calcPY- Price (Clean)

- Yield (%)

- Accrued Interest

- Trading Price

- Discount Rate (if applicable)

Price Analytics

calcPYAnalytics- Approximate Duration

- Approximate Modified Duration

- Approximate Convexity

- PV01 (Price Value of 1bp)

- Yield Value of 1/32

Cash Flow Schedule

calcCFS- Cash Flow Count

- Cash Flow Dates

- Total Cash Flows

- Interest Flows

- Principal Flows

Cash Flow Analytics

calcCFSAnalytics- Yield (Periodic, Semi-Annual, Annual)

- Macauley Duration (Periods, Years)

- Modified Duration

- Convexity (Periods, Years)

- Average Life (Periods, Years)

- After-Tax Yield

- Taxable Equivalent Yield

- PVBPC (Price Value of 1bp Change)

- Total Interest & Principal Flows

- Total IF & PF plus Interest-on-Interest

- Total Interest-on-Interest & Interest-on-Principal

- Total Future Amount

- Total Return (%)

- Capital Gain/Loss

- Total Dollar Return

Coupon Period

calcCouponPeriod- Previous Coupon Date

- Next Coupon Date

Advanced Redemption Controls

The CalculationsFor input allows you to choose which redemption dates are evaluated for callable securities:

Calculations performed strictly to the maturity date.

Determines the Yield-to-Worst and returns that specific scenario.

(Default) Returns both the Yield-to-Worst and Yield-to-Maturity results.

Returns calculations for every call date in the schedule and maturity.

Ready to start integrating? Explore our technical documentation and samples.

Use of the APIs is governed by our .